Moll Properties Apartment Rentals in Ithaca, NY

Home

Now Renting

Parking

About Us

OUR PROPERITIES

Tenant Testimonials

TENANT INFORMATION

Move In

Tenant Portal

Sublet Policy

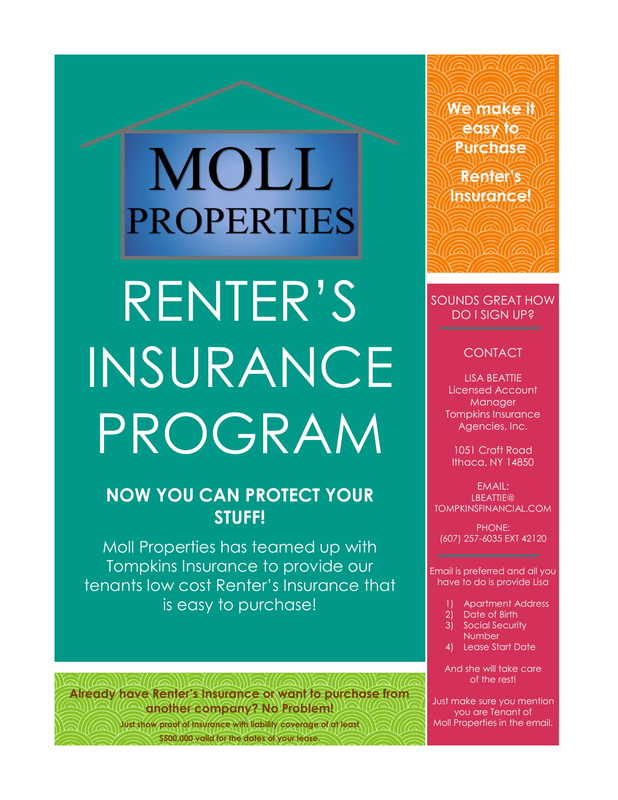

Renters Insurance

Home

Now Renting

Parking

About Us

OUR PROPERITIES

Tenant Testimonials

TENANT INFORMATION

Move In

Tenant Portal

Sublet Policy

Renters Insurance

EMAIL LISA BEATTIE NOW!